Long standing data availability & accuracy challenges take on new imperative with the proliferation of VAT digitalisation and live transaction reporting

The whirlwind of global e-invoicing and digital reporting mandates is upon us as governments demand live access to transactional data to validate and surface errors or even fraud. This means the long-standing challenges around data availability and accuracy must be taken on to ensure business are ready for real-time validations and audits of their transactions.

In this first of two blogs, I’ll be covering the components of the data availability gap. You can read the second, covering the obstacles around VAT accuracy here. And, to give you ideas how to take on these twin stumbling blocks, some help from me. Including our VAT Auditor fast-to-deploy transactional validation product – more details at the end of this blog.

Data Availability + Data Accuracy – need your urgent attention

It may not feel like it for those that are working on some of the newer compliance mandates already, but we are only just at the starting line for this. There has been rapid growth in country specific transactional reporting, immediate filing and e-invoicing initiatives but so far these have primarily been domestic in nature and the vast majority of e-invoicing mandates have been around four corner models that do not include tax authorities in the transaction but rather focus on the standardisation of invoices. As we see moves to include digital reporting for cross border and start to see the evolution of e-invoicing into 5/6 corner models, that do include the tax authority in every invoice issued, companies’ tax data will become critical to their very business existence.

Even without increased transparency a company that does not have a clear grasp of the data that underpins VAT is exposed to unnecessary risk, will be unable to quickly adapt to the changing business world and won’t be able to run efficient tax operations.

There are two main data issues that companies urgently need to get a grasp on:

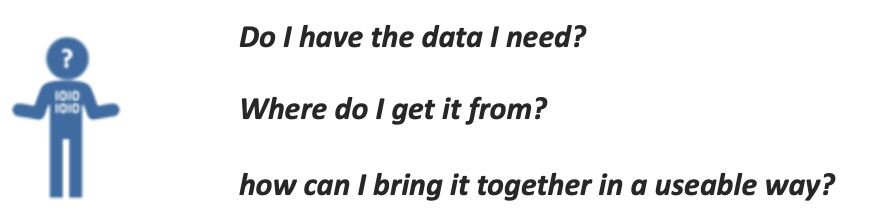

Data Availability

This relates to how easy it is to get the data that is needed to be compliant for VAT, and comes with three questions:

Data availability is consistently one of the hardest problems for tax to solve because the data required for even basic VAT compliance may not be collected, may be spread across multiple parts of their systems and processes, stored across multiple systems in different ways or simply not supported by their systems at all.

This is compounded by the fact that most systems are not built with tax in mind so even if the data exists, extracting it in a useful way is often very difficult.

Some of the key barriers to putting together good tax data are shown in red in the diagram below:

![]()

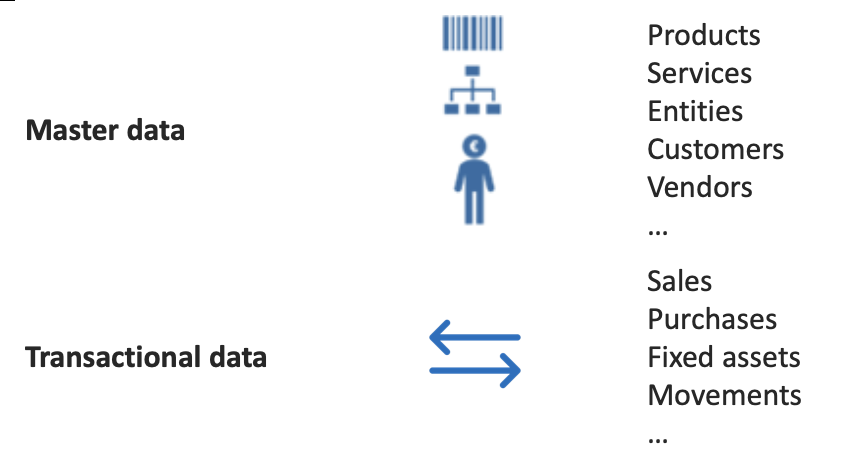

The data needed for tax falls into two categories:

1. Master data

1. Master data

It’s not unusual for companies to have a poor picture of their own entities master data from a tax perspective so imagine how little data may be usefully held about their business partners and the things they supply. This means that no matter how good the technology and processes are for applying and reporting VAT to their transactions they cannot expect to be accurate if they don’t know enough about the taxable entities and taxable transactions.

One of the most common issues is that companies don’t hold or structure the right VAT registrations for their business partners and so they apply the incorrect VAT registrations to their invoices. This has a major impact on the ability for their counterparties to reclaim VAT correctly. This seems like an easy thing to get right but sales and even purchasing teams don’t understand the need to collect and use this type of data properly and their systems are not designed to facilitate it. This is a simple example but determining the correct VAT treatment with precision no matter how you do it requires accurate and detailed data. Going deeper, how many companies hold data about their customers and vendors establishment statuses? This is a critical piece of data for a good tax decision; how can I work out how to tax a B2B service if I don’t know where my customer is established? Nevertheless, the answer is that probably close to zero companies hold this data and rely instead on making high level assumptions.

Five years ago you couldn’t speak to VAT person or a consultant without hearing the term “tax data warehouse”. This is because everyone knew they don’t have the tax data they needed and were looking for a good solution. However, in general none of these projects have been especially impactful and big initiatives of this nature have fallen out of fashion. I believe the primary reason for this is that they are just too late in the process to be useful. The deals were done, the goods were shipped, yeah the data wasn’t properly captured but the sales person got to buy a new watch and it’s all forgotten by everyone except tax & IT who nobly tried to scramble data together into a warehouse to make sense of it after the fact.

What companies really need is for this data to be contemporaneous with their business activities. This is especially apparent in the brave new world of real-time compliance. Tax and IT need to start planning technology projects to record, maintain and make available detailed data for tax within their transactional systems or in services that provide real-time data capabilities at the same time as the transactions occur.

2 Transactional data

Having accurate transactional data has always been important from a supply chain perspective because companies needed to make sure they sent the right thing to the right customer in the right place but data this has never been structured around the needs of tax. As we move to transactional compliance this is become ever more apparent since there is more and more data being needed on every transaction for tax purposes.

Tax codes are no longer enough

Most if not all companies rely on using tax codes to describe the tax treatment and rate of a given transaction. Although it is a headache to build and maintain tax code codes, with companies often needing hundreds if not thousands of codes to encode all the different treatments they have on their sales and purchases around the world, this has been broadly manageable in a world of summarised tax returns. However, as we move to a world where the specifics about a taxable transaction are required for reporting purposes tax codes will not be enough. Companies will need all the underlying data about a transaction to be available.

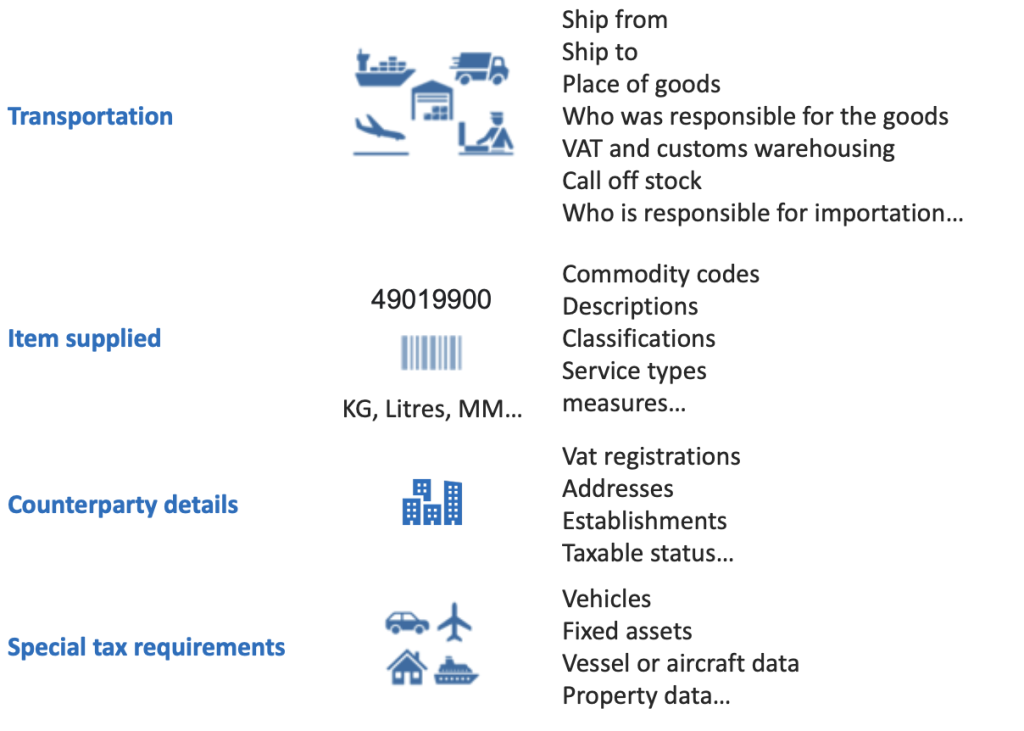

The list is very long but consider whether you have easy access to the data to report on even the basic areas such as:

Many companies barely record enough data to feel comfortable they can generate an accurate summary level tax return. So having to comply with complex requirements with hundreds of attributes like e-invoicing or producing a Standard Audit File for Tax (SAF-T) when requested will prove a herculean task for many companies. Usually, they will have a horrible time pulling the data together and will end up making lots of assumptions and applying questionable defaults that expose them to cost and risk.

Data access

Getting access to the data that is recorded is usually painful too. Data is structured in ERP systems to facilitate the efficient operation of business processes and not for tax so the data needed will often be spread across multiple modules such as sales, logistics, purchasing, global trade and finance modules and is hard to bring together.

Out of the box tax reporting is usually summarised and limited to the point that it cannot be used without significant enrichment.

The technology used often doesn’t support tax needs either with very limited ways to get at the data programmatically with IT often needing to connect to multiple data sources to bring together a meaningful dataset. Even recent attempts by the most sophisticated ERP companies to expose API endpoints for tax haven’t helped much since they usually miss basic tax attributes and insufficient focus is given to improving and maintaining them.

Just getting onto the IT roadmap for changes and support can be a major challenge for many tax teams with lengthy lead times and a lot of work required to justify the priority for system changes that tax needs. This often means that tax has to settle for just enough IT support to maintain business as usual and cannot start to prepare for the digital compliance challenge.

What can VATCalc do to help?

There is no magic wand that a technology tool alone can wave because good data requires a continuous improvement approach that requires focused ongoing attention but everyone needs to start somewhere. So deciding to take action to start addressing the data challenges and having an agile learning mindset where you expect to encounter unknown issues and understand that proper solutions can only be discovered throughout the journey is a paradigm well proven in the technology space.

VATCalc has an excellent technology solution that can help get companies get started by giving them great insights into where the problems are and by providing solutions to some of the most common issues they find.

VAT Auditor is a powerful SaaS tool that allows companies to easily upload transaction sets and have them automatically reviewed for data availability and data accuracy. It works by running a full legislation-based tax determination against each transaction and comparing the results it calculates with the results in the original data.

This is a great way to get started in the data journey because it can identify what key tax data is missing so you can start planning to address the gaps.

If you want to learn more from me, or the rest of the VATCalc team, on how to develop ideas for your local architecture and national tax requirements, contact us for a friendly chat.