What do the countries resisting the fashion for pre-clearance VAT e-invoicing know

What do the countries resisting the fashion for pre-clearance VAT e-invoicing know? Why are they looking at alternatives?

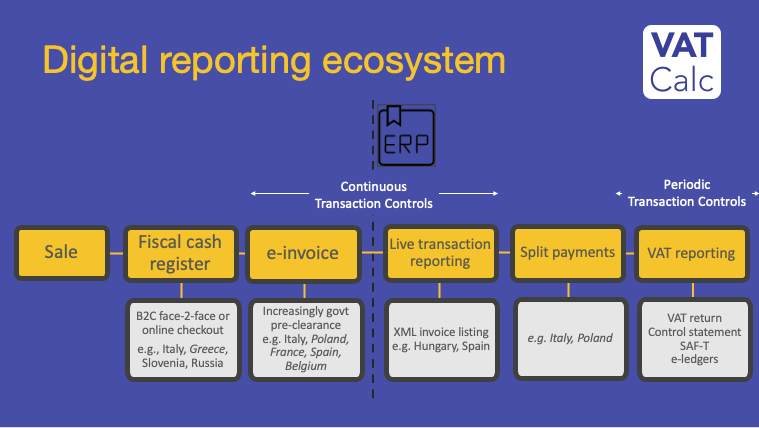

Many European countries are fast-tracking their compulsory VAT electronic invoices plans – often rattled by the pressure of other countries proselytising their own successes with the anti-VAT fraud measure and reducing their VAT Gap. Proposals often include government pre-clearance requirements whereby sales e-invoices must be first submitted to the tax authorities in real-time for digital approval before servicing up the invoice to the customer. The success of Italy’s SdI, which claims to have raised billions since its 2018 launch, has encouraged many others.

And it’s turning into a stampede: France and Poland launching their pre-clearance models in July 2024; Israel even sooner in January of the same year.

But others are holding back – notably Norway, the Netherlands, the UK (which has experienced major cost overruns on MTD for VAT) and others. And the EU’s VIDA 2028 proposals are seeking to prohibit pre-clearance models – although plans to do this may be delayed by 1 year. Whilst pre-clearance was effective in the countries suffering from major VAT Gaps, like Brazil and Italy, the cost/benefit may be doubtful elsewhere.

Here’s why the tide on ‘government-in-the-middle’ model of e-invoicing may be turning.

Mandatory pre-clearance e-invoicing – intrusive government

As many companies, particularly multi-nationals, get to grips with are pre-clearance e-invoice mandates, a range of criticism are emerging that is feeding the doubts of states yet to act. These include:

- Pre-clearance e-invoicing models insert extra reporting and integration requirements into complex sales and fulfilment processes, including rewriting the invoicing process with unique sales invoice ID’s or similar digital certification returned by the tax office. When this fails, or is delayed, it can result is haulted deliveries or customs clearance.

- For services, particularly continuous supplies, invoicing can take place many days or more after the provision of the supply – e.g. telecoms and utilities. Where authorities have imposed live invoice reporting to this use case, businesses end up producing two invoices – an e-invoice for the authorities and a traditional invoice later for the customer.

- Tax authorities have been tempted into demanding additional information on mandatory e-invoices compared to traditional invoices. This can include shipment details or payment settlements. Most of this information is outside of the invoicing ERP or billing applications. This imposes major new IT designs and builds for businesses to provide information of questionable value in the fight against fraud.

- Any electronic data system is vulnerable to hacking or other data leaks. Creating complex, multi-fail point regimes for e-invoices will inevitably heighten the risk of major data losses and related damages for businesses and customers.

- Tax authorities setting the legal framework for e-invoicing will limit the opportunity for development of new invoicing methodologies or technologies that promise better and more efficient exchanges. Governments have a poor track record at picking the best technologies; plus then locking-in suboptimal methodologies.

- When looking at the span of unharmonised pre-clearance regimes, the lack of reusability of technologies (code, connectors and business processes etc) is creating a barrier to cross-border trade and holding back a richer offering of suppliers for customers.

Countries consider the more proportionate alternatives to tackle fraud

As more countries rollout their pre-clearance e-invoice mandates, the above challenges are making other jurisdictions pause for thought. The original aim of VAT e-invoicing – tackling VAT fraud – is being buried under a huge and expensive IT rebuilds for otherwise compliant businesses. This, plus emerging technologies, has prompted several countries to recently declare they have no plans to mandate VAT e-invoicing.

Alternatives are emerging in a mix of digital transaction reporting and Artificial Intelligence

- Digital transaction reporting – is post-ledger posting reporting of transactions. This can be done a few days after transaction posting into ERP’s or similar. It can often just be key data points to help identify VAT fraud (VAT ID’s; amounts; dates; VAT calculations etc) rather than full invoice data. Aside from assuaging privacy and security concerns, this keeps all the requirements within the basic invoicing natural or native systems and so relatively simply to implement. The EU’s VAT in the Digital Age proposals for Digital Reporting of intra-community supplies partially reflects this changing mood.

- Digital bookkeeping – including mandating certain standards of accounting, EPR and invoicing systems. This includes Denmark e-record keeping, which adapts existing natural / natives systems to full digital standard and audit requirements. Ideally, this should include e-invoicing support based on Peppol and similar standards.

- Artificial Intelligence in tax authorities is already a well established success story. Its ability to identify anomolies in huge voluments of transaction data, including bringing in other comparative sources, has meant that it’s been adopted by over 50 jurisdictions already. AI closing the VAT Gap can provide tax staff with customised functionalities to analyse intricate, multi-layered relationships between entities in transaction data during audits or investigations. It can also uncover relationships more than 10 connections deep across various public information sources in a real-time manner.

The expectations for this pairing are very high. Particularly when the implementation timetable for pre-clearance e-invoicing is a minimum of three years. France’s e-invoicing will be six years.

The pace of technological advancements in low-cost AI is now encouraging a growing number of tax authorities not to be panicked into the cost and disruption of pre-clearance by their noisy neighbours.

CTC e-invoicing and real-time models

| Invoice reporting model | Examples | Features |

| 1. Central platform exchange | Italy, Turkey | Platform responsible for invoice forwarding to customer |

| Customer or receiver may review and reject invoice | ||

| 2. Central clearance | Govt platform accepts invoices, validates, and buyer acknowledges invoice | |

| Brazil, Colombia | Pre-clearance variation - clearance before invoice exchange | |

| Chile, Costa Rica | Post-clearance - clearance short time after exchange | |

| Document types not regulated and therefore inconsistent and may resort to email and similar | ||

| 3. Decentralised clearance | Mexico, Guatemala, Peru, France | Certified e-invoice agent (PAC) submitts inoices |

| Document types not regulated and therefore inconsistent and may resort to email and similar | ||

| 4. Real time digital reporting | Spain, Hungary, South Korea | Invoice listing submitted immediately after invoice issued |

| No acceptance or regulation of invoice by tax authorities |