MyInvois portal 1st Aug 2024 launch given 6-month option to submit invoices 7 days after month end

The Malaysia Revenue Board has granted a 6-month soft landing for its 1st August 2024 MyInvois live e-invoicing mandate. Taxpayers in the first wave (turnover above MYR 100m) will not be obliged to pre-clear their invoices from 1 August 2024. Instead, they may use current invoice formats and digitally report the transactions in a single submission by the 7th of the following month. This means the first digital transaction reporting deadline will be 7th September 2024. This optional post invoice issuance digital reporting phase will end 1 February 2025 when the penalty regime for not reporting live via MyInvois will be imposed.

Taxpayers that voluntarily start using MyInvois live reporting from 1 August will be entitled to accelerated capital allcowances on related IT spend.

This period of flexibility is expected to give a space of time sufficient for taxpayers to ensure the implementation of e-Invoicing fully which is more effective covering all aspects such as system availability, smooth business operations and change management in business.

25th July 2024 – new FAQs and guidance

The Ministry of Finance Inland Revenue Board of Malaysia (LHDN) issued updated Frequently Asked Questions and guidance for the 1st August 2024 launch of its MyInvois e-invoicing regime. The FAQs are for 19th July 2024, and the guidance is version 3.1 with updates on INCOTERMS and product tariff codes.

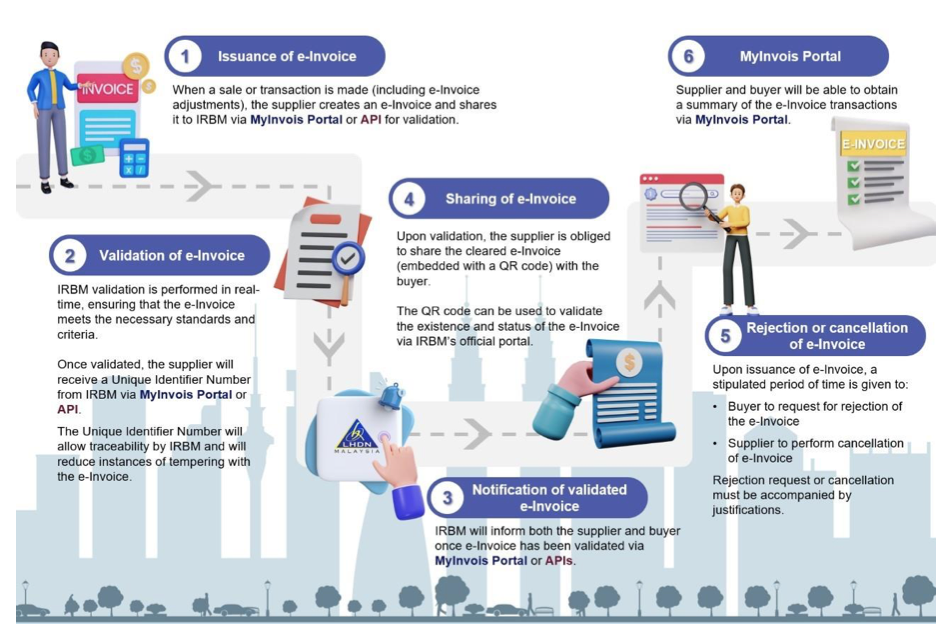

The timetable for the pre-clearance electronic invoicing regime is:

- 1 August 2024: taxpayers annual turnover above MYR 100 million (approx $21m) – about 4,000 taxpayers;

- 1 January 2025: taxpayers with annual turnover between MYR 25 million (approx $5m) and MYR 100 million;

- 1 July 2025: all other taxpayers

This requires sales invoices to be generated in the form of XML or JSON file format, in accordance with the requirements outlined by the IRBM. Refer to e-Invoice Software Development Kit (SDK) Microsite.

MyInvois is the solution of the LHDN used by taxpayers to submit their issued documents with the tax authority, get notified on events related to document issuance. This site contains documentation of the APIs exposed to taxpayer ERP systems that can be used to integrate with MyInvois System to automate the document processing.

Need help complying with the new Malaysian requirements? A simple, and quick connection from your ERP, marketplace or invoicing system to our VAT e-invoicing product is all that is required. This can cover you for Malaysia, Singapore, Australia, New Zealand, Indonesia and Japan. Contact us to learn more.

Malaysia will operate a Continuous Transaction Control CTC model, requiring sales invoices (XML) to be first sent to the tax authorities for verification via the government’s API. Once approved, the invoice is given a unique digital Certification Serial Number. Once returned to the seller, only then can it be sent to their customer in any format. There will be a PEPPOL option for this exchange of invoices. A QR Code must be included with the invoice sent to the customer.

For B2C, transactions where e-Invoices are not required by the end consumers to support the said transactions for tax purposes, suppliers will be allowed to issue a normal receipt or invoice in accordance with the current practices adopted by suppliers. After a certain period or timeframe, suppliers would be required to aggregate the normal receipts or invoices issued to end consumers and issue a consolidated e-Invoice to support the transactions made with end consumers. Further guidance on this will be provided in due course.

This is part of a broader digitisation of tax administration. A pilot will kick-off at the start of 2024 with a phased introduction for other taxpayers during the rest of the year.

This is part of a broader digitisation of tax administration. A pilot will kick-off at the start of 2024 with a phased introduction for other taxpayers during the rest of the year.

E-invoicing has been permitted in Malaysian since 2015. Both parties, the vendor and customer, must be in agreement. Electronic invoices should be retained for at least seven years.

VATCalc’s international live VAT invoice transaction and e-invoice tracker on real-time transaction-based tax reporting lists all the countries imposing transaction-based reporting.

Malaysia had introduced a full VAT regime – termed Sales and Services Taxes – between 2015 and 2018. But it returned to the old sales tax, Goods and Services Taxes. It is likely that Malaysian GST will return.

[/vc_column_text]