Following the ending of the UK’s Brexit transition period on 31 December 2021, the standard Value Added Tax return has undergone some minor changes.

Updated VAT return to reflect leaving the EU

This reflects the UK being outside of the EU VAT regime, meaning:

- Movements of goods between EU and the UK are no longer intra-community dispatches and acquisitions – instead they become exports and imports, respectively

- UK importers may defer the UK import VAT due on clearing EU goods into the UK under the postponed VAT accounting option. This is done via the reverse charge.

- Northern Ireland now holding a dual position within the UK and EU VAT regimes

- UK e-commerce businesses no longer being able to use the distance selling VAT thresholds to sell to EU consumers under the UK VAT number

If you need to complete UK post-Brexit VAT returns, VAT Calc’s VAT Filer can correctly complete any country filings with verified VAT or GST transactional data from our VAT Calculator or VAT Auditor tools.

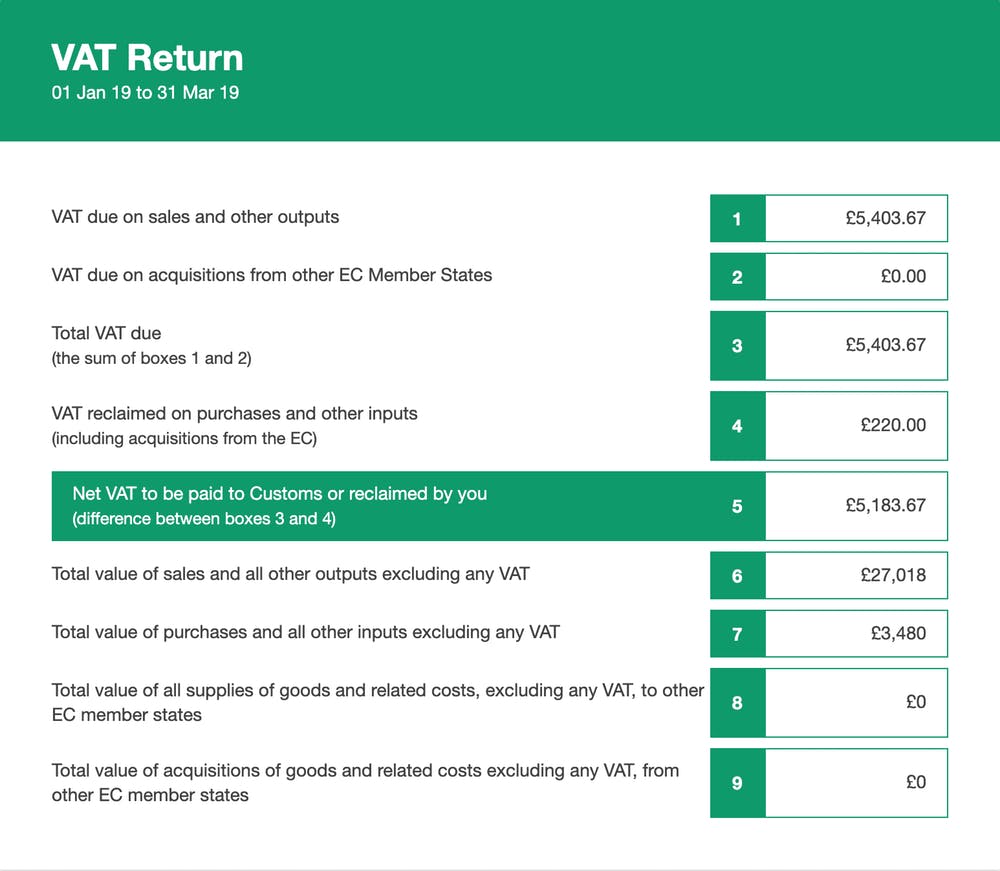

The same nine boxes remain, and disclosures are as follows:

| Box | Post-Brexit declaration |

| 1 | VAT due in the period on sales and other outputs

Continue to include any VAT due to HMRC in box 1 of the VAT return. If you using Postponed VAT Accounting (PVA), the import VAT payable should be declared here. Supplies of services within the reverse charge will continue to be declared in box 1. |

| 2 | VAT due in the period on acquisitions of goods made in NI from EU Member States

Since 1 January 2021, the only acquisitions you include in box 2 are acquisitions of goods from the EU to NI. |

| 3 | Sum of boxes 1 and 2 |

| 4 | VAT reclaimed in the period on purchases and other inputs (including acquisitions from the EU)

VAT to be reclaimed as input tax will continue to be entered in box 4. If you are declaring import VAT via PVA, you will also reclaim the import VAT on the same VAT return via box 4, to the extent your business is entitled to recover this VAT. If you are reclaiming import VAT using a C79 (the import VAT certificate issued by HMRC) , you will enter the import VAT amount stated on the C79 once received. Supplies of services within the reverse charge will continue to be reclaimed in box 4, again to the extent your business is entitled to recover this VAT. |

| 5 | Net to pay HMRC (box 3 minus box 4 |

| 6 | Total value of sales and all other outputs excluding any VAT

The net value of all supplies of goods and services including supplies of goods and/or services to both business customers and private individuals outside the UK. |

| 7 | Total value of purchases and all other inputs excluding any VAT

The net value of all purchases of goods and/or services should be included including reverse charge transactions. |

| 8 | Since 2021, only enter the net amount in box 8 if trading in NI and supply goods to EU Member States. Figures in this box must also be entered in box 6. |

| 9 | Since 1 January 2021, only acquisitions of goods from an EU Member State into NI will be entered in box 9. Figures in this box must also be entered in box 7. |

For temporary imports, VAT and duties refunds on Inward Processing is a good cash flow option.