ECJ ruling on EU triangulation VAT invoicing underlines need for correct ‘invoice mentioning’ to avoid lost VAT

The December 2022 European Court of Justice ruling on C-247/21 (Luxury Trust Automobil) has underlined that the invoices used to report the triangulation simplification must clearly refer to the appropriate legislative articles or face VAT liabilities.

The case concerned three businesses making use of the triangulation simplification. The intermediary, based in the Czech Republic failed to refer in its invoice to the final Austrian customer that it was relying on Austrian triangulation. It did not contain a reference to the transfer of the tax liability (Article 25(4) of the UStG 1994) to the Austrian customer and that it should report the VAT. The Czech intermediary was therefore considered a ‘missing trader’ for VAT fraud by the Austrian authorities. They considered the transaction to be a ‘failed triangular transaction’ that cannot be remedied after the event. The Czech sellers was held liable for VAT on its invoices to its Austrian customer.

The ECJ judgement confirmed this: the final (Austrian) purchaser has not been effectively determined as the VAT debtor in the context of a triangular transaction if the invoice issued by the intermediate (Czech) purchaser does not contain the information “tax liability of the service recipient” in accordance with Art. 226 No. 11a of Directive 2006/112 as amended.

Crucially, the ruling did not allow for the post-event correction of the invoice, a ‘material effect requirement’, and this departs from typical decision.

Our VAT Advisor also covers cross-border chain transactions.

At VAT Calc, because we’re unique in being built on EU VAT Directives and local tax law variations, we have this fully automated. That means our tax engine, VAT Calculator, can ensure you’re using the right VAT numbers in your Triangulation transactions, and that you’re following local variations. In addition, the engine understands the rules around transport responsibility so the simplification will only apply when the necessary conditions are met.

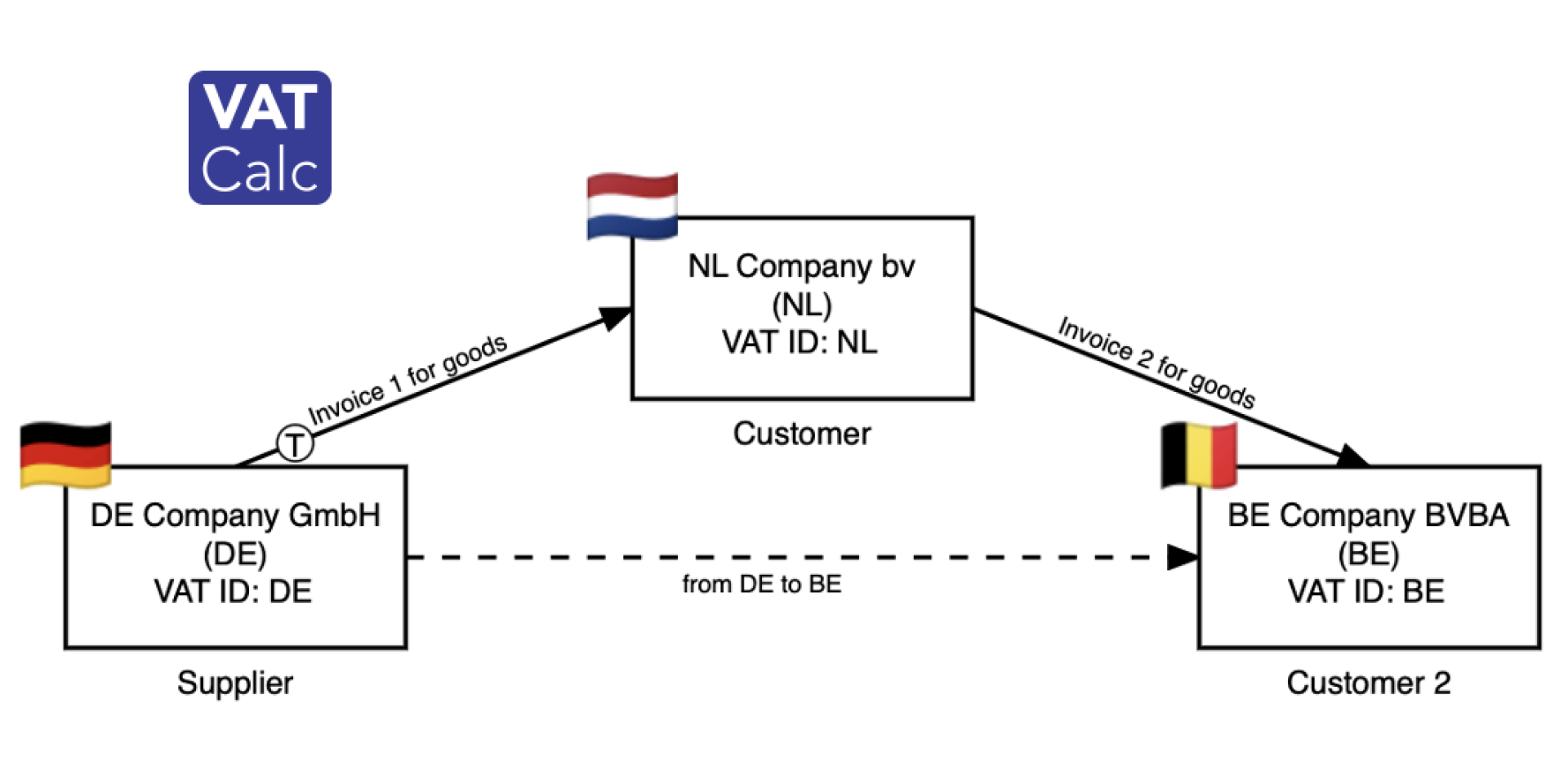

How does Triangulation work?

Triangulation applies between three companies using VAT ID’s in three different EU Member States, involved in successive supplies, with 1 cross-border transport of goods between the first supplier and the last customer. See below.

The Intermediary, in The Netherlands, has a customer in Belgium. It sources the goods from its Supplier in Germany. Ordinarily, the Intermediary would have to VAT register in Belgium to account for VAT on the arrival of the goods from Germany and then also on the sale to the Customer in Belgium. However, Triangulation, under Article 141 of EU VAT Directive, exempts the VAT on acquisition. The VAT on supply by the Intermediary in Belgium is declared by the Customer under the reverse charge mechanism per Article 197 of the VAT Directive. As such, the Intermediary avoids VAT registration in Belgium. The Intermediary will, however, need to report these transactions on an EC Listing.

Transport complications for Triangulation

There is a complication on the above in the event that the Customer is responsible for the transport. Under triangulation, the transport is allocated to Invoice 1 on the supply to the Intermediary (Article 36a EU VAT Directive). But if the Customer, and not the Intermediary or Supplier, is responsible for the transport then this will likely invalidate the use of Triangulation.

Simplified triangulation country rules

But what happens if the Intermediary is VAT registered in the country of destination. Should they use these numbers or do they use the Triangulation route?

The answer depends on the EU member states as they have varying rules. If the country does not allow Triangulation if the Intermediary is registered in Country C, then the Intermediary should instead use that local VAT number, charge and collect VAT. Additionally, where local rules prohibit the Intermediary from holding a VAT number in country A, the simplification cannot be applied.

This is despite the ECJ Case C-580/16 (Hans Bühler) judgement which permits traders to choose a VAT registration number to apply. Previously, some tax offices refused the simplified triangulation rules if the Intermediary had a VAT number in the country A, the country of dispatch. The Intermediary consequently still has to register for VAT in country C. This case means that the simplified triangulation rules can still be applied, provided that the Intermediary ‘acquires’ the goods under a VAT number of an EU Member State other than the Member State of dispatch. The Intermediary therefore does not have to register for VAT purposes in the EU Member State of arrival.

However, a number of countries have not implemented this in their local laws.

Which countries still apply differing rules? Our VAT Calculator tax engine includes all of these variations. As you submit your transactions to the application, and VAT registrations of parties, it will indicate the correct VAT number to use on the transaction apply and whether Triangulation simplification may be applied given the Member States’ application of the rules. And, lastly, these are then all posted without further effort by you to the right boxes in each countries’ VAT return via our VAT Filer, built on the same application as VAT Calculator.

EU Simplified Triangulation by state

| wdt_ID | EU state | If Intermediary registered in country of dispatch? | If Intermediary registered in country of arrival? |

|---|---|---|---|

| 1 | Austria | Yes | No |

| 2 | Belgium | Yes | Yes |

| 3 | Bulgaria | Yes | Yes |

| 4 | Croatia | No | Yes |

| 5 | Cyprus | No | No |

| 6 | Czech Republic | Yes | No |

| 7 | Denmark | Yes | Yes |

| 8 | Estonia | Yes | No |

| 9 | Finland | Yes | Yes |

| 10 | France | Yes | No |