March 2028 VAT on all import B2C consignment must be charged at sale in checkout; IOSS €150 limit withdrawn; marketplaces liable for seller VAT and customs; optional Special Arrangements extended

As part of yesterday’s EU Customs reforms proposals, the VAT special arrangements threshold of €150 is to be withdrawn too. The Customs reforms proposes scrapping a similar customs duties threshold of €150 which was blocking the VAT threshold ending.

2028 – Five e-commerce changes to EU VAT Directive

The European Commission if proposing the following changes to the EU VAT Directive in relation to imports of goods to consumer and the July 2021 e-commerce VAT package:

- VAT and customs will be charged in the checkout for all import consignments exceeding €150, not just on sales below this threshold for VAT, as today.

- To support this customs duties reporting and payments, a new ‘deemed importer‘ concept is being created for any party importing B2C consignments from outside the EU and who may use the IOSS regime. They will also be allowed to use IOSS to settle the customs debt and apply a simplified tariff treatment for sales made to consumers when determining the appropriate customs value.

- Where a marketplace has facilitated this sale, it becomes liable as the deemed supplier for the VAT and customs charges and collection. Platforms are today only liable for sales not exceeding €150. Note: today, platforms are not obliged to accept this liability, but under the VAT in the Digital Age reforms, they will be from January 2025.

- Sellers or marketplaces affected by the above may use the e-commerce package Import One-Stop Shop return to report these sales. Currently, they are limited to sales not exceeding €150.

- The e-commerce package optional Special Arrangements will be extended to consignments above €150, too. These allow an option whereby postal operators, express carriers, customs agents, and other operators who fulfil the customs import declarations on behalf of the customer are allowed to declare and remit the collected VAT on those imports on a monthly basis.

Our VAT Calculator tax engine can provide instant e-commerce sales calculations for your checkout, and VAT Calc’s single platform VAT Filer can accurately complete the IOSS with verified transactional data.

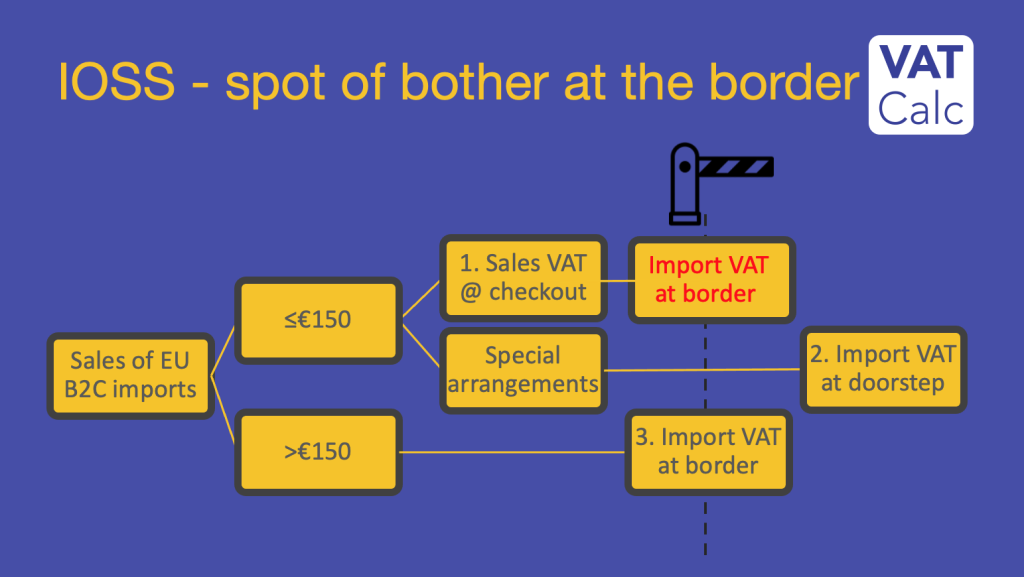

Ending IOSS double taxation risk on imported consignment stocks

The above changes will help tackle the problem of double taxation on consignment stocks which may today be taxed both at the checkout and then secondly at the customs border.

As shown below, a second charge of import VAT (marked in red) may be charged on importation of consignment sales to consumers in addition to the charge of sales VAT @ checkout.

Member States shall adopt and publish, by 31 December 2027 at the latest, the laws, regulations and administrative provisions necessary to comply with this Directive. They shall forthwith communicate to the Commission the text of those provisions.

They shall apply those provisions from 1 March 2028.