ViDA: Extension of OSS return for cross-border movement of: own goods; B2C e-commerce; and B2B call-off stock. Likely delay to 2026

Harmonisation of B2B reverse charge. But extension of marketplace ‘deemed supplier’ to EU sellers proposal now dropped

The proposed 2025 adoption – now likely delayed to 2026 – of the existing One-Stop-Shop OSS VAT return to further B2C and B2B stock movements is at the core of the Single VAT Return pillar of VAT in the Digital Age. The other two pillars are: Platform Economy 2025; and Digital Reporting Requirements delayed to 2030.

Extension of OSS for B2C and B2C own stocks

- The e-commerce package success of One-Stop-Shop VAT return for distance selling will be extended to movements of own stock by e-commerce sellers prior to B2C e-commerce sale (B2B2C transactions).

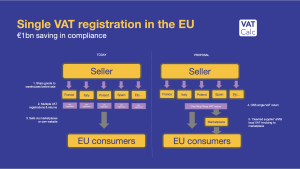

- The SVR will enable businesses to charge, report and manage their entire EU VAT through their domestic tax authorities, including eventually the entire audit process.

- The stock movement remains taxable with two transactions – arrival and sale. Both would be reported in the OSS, which would need additional information added to be reported to the member state of indentification (where OSS is registered).

- This will eliminate the need for hundreds of thousands of foreign VAT registrations for e-commerce sellers. The EC estimates that managing each single foreign registration costs €5,000 per annum for businesses. This change in total will cut sellers’ cost by €800m per annum or €8.7bn between 2023-32 estimates the EC.

- The current €10,000 pan-EU distance selling threshold will be limited to where the seller is established. So they may not use it a second+ time if they hold stocks in other member state territories.

- Other B2B transaction where excluded for the 2025 implmentation were excluded because of the problems of deductibility. But this may change in the future.

Original proposal for Marketplaces deemed supplier extending to EU sellers now dropped

- For EU sellers, where cross-border e-commerce sales are facilitated by a marketplace, the VAT on the local domestic sale to the consumer was to flip to the marketplace as the deemed supplier. The exception is sales in the country where the seller is resident.

- This has now been put aside for the future.

- The seller will use OSS to report the zero-rated taxable acquisition to the marketplace.

- B2B transactions under the scenario would be zero-rated for VAT.

- The disadvantage of this decision is that it would favour sellers using marketplaces and penalise own website sales which would still be responsible for the domestic VAT reporting.

OSS Special scheme for movement of own goods

- Plus, under OSS for other own stock movements there will be a special scheme within OSS. The intra-Community acquisition of goods in the Member State where the goods are dispatched or transported to, is exempt. This must be supported by detailed records. The existing call-off stock provisions of the EU VAT Directive will therefore be withdrawn from 1 January 2025 for new movements as no longer required with OSS. Existing stocks already held in call-off stock will still follow the current rules until 31 December 2025.

- There will be ring fence exceptions with right of deduction e.g. cars; capital goods; and non-saleable company assets.

- In addition, traditional cross-border services where the seller is not resident will be added to OSS option, which includes: Installation and assemble of goods; goods made on board means of transport; goods supplied at exhibition or trade fairs; goods at weekly markets; and local hire of transport.

- Purely B2B transactions are not included for the time being in this extension because of the complexities of right of VAT deduction and fraud risks

IOSS updates – Jan 2026?

- There were three important modifications considered for the Import One-Stop-Shop which was introduced under the 2021 e-Commerce VAT Package:

- The current €150 consignment threshold for imported B2C sales will NOT be raised in the immediate future. It will likely be postponed until the Customs processes and requirement can be reformed, too.

- IOSS will be mandated for marketplaces to cut down fraud and errors.

- As an anti-fraud measure, a link between IOSS numbers and consignment stocks

- Other quick fix improvements to IOSS double taxation issues are included.

B2B Reverse charge optional for non-residents

- Change to reverse charge for non-established sellers. A standardisation across the member states of the rule when the buyer has a VAT number in the country of supply. The use of the simplification will become optional for businesses.

- This will provide certainty for businesses, but increase the instances where a foreign vendor can rely on the reverse charge and not have to VAT register in a country where they are selling.

- This has been included partially as the extension of OSS did not go as far as to allow B2B sales.

Extension of OSS to other cross-border services when the seller is non resident

Aside from transfer of own goods, a range of B2C cross-border transactions will also potential now be included:

- Installation and assemble of goods

- Goods made on board means of transport

- Goods supplied at exhibition or trade fairs

- Goods at weekly markets

- Gas, electricity and heating

- B2B supplies of services where there is a ‘may’ option on using the reverse charge

- Immovable property

- Passenger transport services

- Admission to cultural, sporting, exhibition etc events

- Restaurant and catering

- Short-term transport hire

VAT Filer reporting for OSS extension

VAT Calc’s global returns reporting app, ‘VAT Filer’, has been developed with the EU’s VAT in the Digital Age reforms in full focus, the extension of OSS for own stocks and other supplies. And since VAT Filer is built on the same single platform as our VAT Calculator tax engine product, there is full reconciliation on VAT return reporting.

EU VAT in the Digital Age reforms

| EU VAT in the Digital Age | |

| 3 pillars to improve efficiency of VAT for all and reduce fraud | |

| 1. Digital Reporting Requirements; e-invoicing | 2030?: Mandatory digital reporting of intra-community transactions; obligation to be able to issue and receive intra-community e-invoices; member states free to impose own e-invoicing or real-time reporting but most conform to EU e-invoice standard EN 16931 |

| Read more about EU Digital Reporting Requirements (DRR) | |

| Structured e-invoices mandated for intra-community supplies | |

| EC Sales lists replaced by Digital Reporting Requirements | |

| Withdrawal of EU permission requirements for e-invoicing | |

| 2 Platform economy | 2025: Travel & accommodation sharing platforms to become deemed supplier / liable to users' VAT. New definitions of the roles of providers, users and platforms to avoid double and no-taxation |

| Read more - Travel & accommodation platforms deemed suppliers for EU VAT | |

| 3 Single VAT Registration; extension of OSS | 2025: Following the 1 July 2021 introduction of the One Stop-Shop (OSS), extended to cover movement of own stocks prior to cross-border B2C to reduce the foreign, non-resident VAT registrations & returns. Plus to movements of own stock with ending of 'call-off' stock burden |

| More details on Single VAT Registration in the EU | |

| Marketplaces deemed supplier for EU sellers | |

| EU IOSS mandated for marketplaces | |

| EU tackles misuse of IOSS numbers | |

| Quick fixes to existing e-commerce VAT rules | |

| Call-off stock VAT simplification ends | |

| Harmonisation of B2B Reverse Charge rules | |