ViDA Pillar 1, Digital Reporting & e-invoicing, postponed to 2030 or 2032

Plans to gain political agreement of the 3-pillar VAT in the Digital Age reforms this year set to hit delays. Ongoing efforts to find compromises on pillar 1 Digital Reporting Requirements and e-invoicing, are delayed to next year, and implementation date shifted from 2028 to likely 2030 or even 2032.

The EU Parliament ECON has voted on 23 October for a one-year delay to all 3 ViDA pillars. However, this is non-binding but reflects the concerns for businesses and tax authorities be ready for the reforms.

2-year delay and further amendments to original EC’s ViDA DRR proposals

-

- Delaying initial 2024 proposed reforms, including: ending requirement for EC approval on e-invoicing; obliging all companies to be able to receive suppliers e-invoices.

- Allowing member states to continue in full with their own existing domestic VAT pre-clearance regimes. So no harmonisation of domestic regimes with the EU-wide DRR. Once Pillar 1 is introduced, no further pre-clearance models may be adopted;

- Buyers will retain right to refuse e-invoicing format.

- Payment details to not include sequential numbering; IBAN payment details (other details to be included); or payment date

- Lengthen the proposed 2-day transaction reporting and e-invoicing deadline for intra-community transactions

- Withdrawal of EC’s proposal to prohibit summary invoices

- Following the planned French e-invoicing, allow ‘certified private platforms’ model for member states to choose. So moving from central reporting to a distributed ‘Y-model’. Also, perhaps the option of certified software to issue approved e-invoices – following the Denmark plan.

Orignal DRR proposals now delayed

The European Commissions proposed Digital Reporting Requirements (DRR) includes two paths to tackle help tackle the EU VAT Gap. It is part of the three pillar VAT in the Digital Age package.

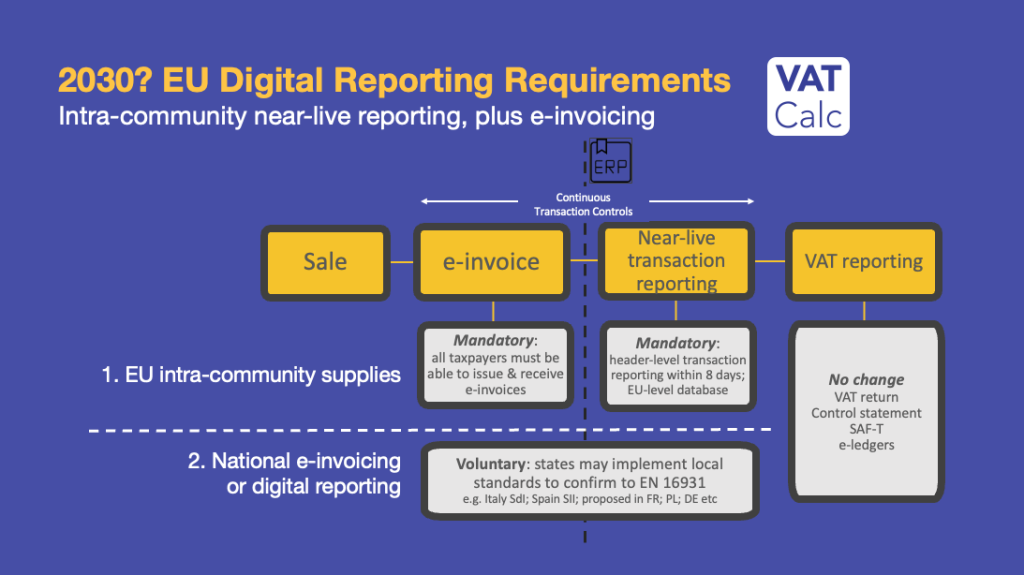

1. Mandatory B2B Intra-community digital reporting requirement (DRR) near-live reporting ICS supplies & acquisitions; replacing EC Sales Lists summaries

-

- Intra-community supplies (ICS) digital reporting regime will be introduced for all companies, including non-residents, from 2028. This data will be submitted first to the national tax authorities for immediate consolidation in a common EU database with endpoints. However, no reporting technical details for passing transaction data to a central database, Central VIES, has yet been confirmed and will remain flexible for member states but comply with Implementation Decision (EU) 2017/1870.

- There will be a header-level transaction reporting schema based on the European standard for e-invoicing (EN 16931) and so following exiting B2G initiatives. For data protection law reasons, not all the invoice information will be reported. And no pre-clearance of invoices, but Continuous Transaction Control CTC

- However, since tax authorities will be able to cross-check supplies and acquisitions information in Central VIES to identify fraud, this is not necessary.

- Reporting frequency will be within two working days of a chargeable event – so not real-time. The VAT Directive therefore will be amended from the current 45-day limit for invoicing intra-community supplies. Taxpayers may submit the information directly or via 3rd party.

- It would only apply to B2B transactions – intra-community B2C will be excluded for the time being.

- Following EN 16931 will help encourage adoption of the standard by all countries for their domestic digital reporting requirements, improving interoperability and reducing costs for taxpayers since it will be a subset of the above e-invoicing requirements.

- The introduction of the new intra-community reporting regime will enable the withdrawal of EC Sales Lists (ESL), known as recapitulative statements.

- Central VIES – EC operated transaction database

- A new ‘Central VIES’ central database will be overseen and maintained by the EC, and will include DDR transactions and ID info of taxpayers, including their VAT identification number. It will also have some integration into the Customs Surveillance system and the upcoming Central Electronic System of Payment CESOP information

- It will also give transparency for customers to see what intra-EU transactions are being reported against their VAT numbers. This will help prevent them potentially being caught-up in VAT frauds unaware. This may be enabled by a common EC endpoint.

2. Mandatory intra-community E-invoicing; domestic transactions left to member states’ local plans

-

-

- All businesses will be obliged to be able to issue and receive VAT e-invoices for ICS’s based on European standard for e-invoicing (EN 16931) for intra-community supplies. This will be a structured e-invoice format (XML; UBL; PDF/A3 etc) and not PDF’s.

- Further data will be added to existing invoicing information including: IBAN number (or other identifier) of supplier’s account that will receive payment; Payment due date; and if invoice correction.

- Jan 2024: For domestic transactions, member states will be free to remove the obligation for customers to accept e-invoicing from their suppliers to help adoption of domestic e-invoicing.

- States will also no longer have to seek EU approval for mandatory domestic e-invoicing as per the current Article 232 of the VAT Directive. This will require a VAT Directive amendment, Article 218, that electronic invoicing will be the default system for the issuance of invoices. The use of paper invoices will only be possible in situations where Member States authorise them. Summary invoices would also be ended.

- Member states may still adopt their own formats, but will be encouraged to follow or converge towards EN 16931 to help with long-term harmonisation of EU reporting systems. It is therefore not clear yet if or what role there will be for PEPPOL or e-invoicing agents for transmission of e-invoices at the national level. The key requirement is that they are interoperable with the EU plans.

- Jan 2028: Member states will not be allowed to use pre-clearance e-invoice authorisation (mandatory authorisation or verification) on e-invoices. However, where already implemented, e.g. Italy, this may continue until 1 January 2028.

- Member states with existing domestic digital transaction reporting regime will have to converge by 1 January 2028.

-

Tax Engine and VAT reporting with CTC

VAT Calc’s tax engine, ‘VAT Calculator’, has been developed with the EU’s VAT in the Digital Age reforms in full focus, including Continuous Transactions Controls agility to live calculate and report invoice data. And since VAT Calculator is built on the same single platform as our VAT Filer product, there is full reconciliation on VAT return reporting.

EU VAT in the Digital Age reforms

| EU VAT in the Digital Age | |

| 3 pillars to improve efficiency of VAT for all and reduce fraud | |

| 1. Digital Reporting Requirements; e-invoicing | 2030?: Mandatory digital reporting of intra-community transactions; obligation to be able to issue and receive intra-community e-invoices; member states free to impose own e-invoicing or real-time reporting but most conform to EU e-invoice standard EN 16931 |

| Read more about EU Digital Reporting Requirements (DRR) | |

| Structured e-invoices mandated for intra-community supplies | |

| EC Sales lists replaced by Digital Reporting Requirements | |

| Withdrawal of EU permission requirements for e-invoicing | |

| 2 Platform economy | 2025: Travel & accommodation sharing platforms to become deemed supplier / liable to users' VAT. New definitions of the roles of providers, users and platforms to avoid double and no-taxation |

| Read more - Travel & accommodation platforms deemed suppliers for EU VAT | |

| 3 Single VAT Registration; extension of OSS | 2025: Following the 1 July 2021 introduction of the One Stop-Shop (OSS), extended to cover movement of own stocks prior to cross-border B2C to reduce the foreign, non-resident VAT registrations & returns. Plus to movements of own stock with ending of 'call-off' stock burden |

| More details on Single VAT Registration in the EU | |

| Marketplaces deemed supplier for EU sellers | |

| EU IOSS mandated for marketplaces | |

| EU tackles misuse of IOSS numbers | |

| Quick fixes to existing e-commerce VAT rules | |

| Call-off stock VAT simplification ends | |

| Harmonisation of B2B Reverse Charge rules | |