BMF publishes draft high-level letter of regulations for implementation of e-invoicing

The German Ministry of Finance has published on 13 June 2024 a draft letter on the regulations for the upcoming mandate of B2B e-invoicing. This is now in circulation of general feedback until 11 July. It covers the first requirements, from 1 January 2025, the all resident taxpayers must be able to receive structured e-invoices for domestic B2B transactions.

The final publication of the BMF letter is for the beginning of the IV. Planned for the quarter of 2024. The letter covers:

- Current legislative situation – the implementing Growth Opportunties Act

- Types, formats and obligations to issue e-invoicing from 1 January 2025

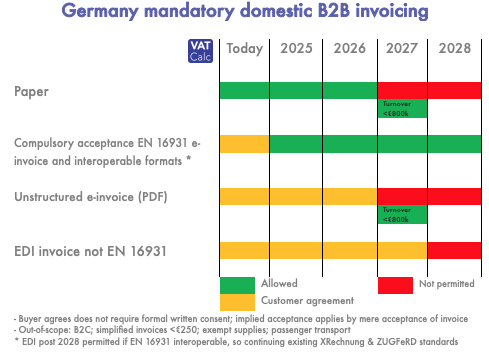

- New definition of a machine-readable structured e-invoice under EN 16931 EU standard or agreed between counterparties that are secure. Some exemptions, including <€250 value.

- Hybrid with XML, XStandard and ZUGFerd qualify

- Attachments may be included to enable contract or similar commercial terms to be added

- Electronic transmission of e-invoice, which may be email (but still structured (not PDF!), portals or service providers. No memory sticks or similar exchanges. So setting-up an email box to receive and store structured e-invoice would meet the Jan 2025 requirements.

- Input VAT deduction considerations as only structured e-mail valid under above requirements.

- Storage issues

- Transitional arrangements see table below:

March 2024 Domestic B2B e-invoicing law gazetted following Bundesrat Federal Council consent

Germany has gazetted on 27 March its Growth Opportunities Act (Wachstumschancegesetz), which includes mandatory domestic B2B invoice phased in between 2025 and 2028 (see diagram below).

Germany’s Bundesrat (Federal Council), consented on 22 March to the legislation, This wide ranging economic stimulus bill was already approved by the Bundestag.

Importantly, the German e-invoicing regime only governs the formats adopted for B2B domestic invoices. It does not (yet!) include government pre-clearance or post-issuance digital reporting. This will change probably 2030 with the EU VAT in the Digital Age digital reporting requirements for intra-community supplies. The existing German XRechnung & ZUGFeRD standards will continue provided they remain interoperable with the new rules.

Council of EU approves mandatory German e-invoicing

The request by the European Commission on behalf of Germany to introduce mandatory B2B domestic VAT e-invoicing was approved by the Council of the European Union on 25 July. This allows Germany to impose real-time e-invoicing which it is now proposing for 1 January 2025 to 2028.

The request was backed by the EU Commission in June (see below) to authorise Germany to derogate from the EU VAT Directive and its requirement for paper-based invoices. Germany will be permitted to impose e-invoices until the end of 2027 when there will be a further review.

Learn about VATCalc’s VAT e-invoicing product, which not only creates and submits e-invoices to global tax authorities, but is unique in providing full audit against local tax legislation. And since it is built on the same application as our VAT Filer, all of your sales or purchase e-invoices are fully reconciled to your VAT returns.

Germany’s application to the EC lasts until December 2027. However, the EU is proposing to remove this requirement to seek its approval to deviate from the EU VAT Directive on e-invoicing from 1 January 2024 (now delayed to probably January 2025. This is part of the ViDA reforms.

This proposal follows a 2022 commitment from the new coalition government to introduce a digital reporting regime to help tackle the VAT Gap.

Germany is to follow Italy, France, Poland and others by introducing mandatory electronic invoices. It has commenced plans by seeking permission from the European Commission to do so – under the EU Directive rules, businesses must first seek their suppliers’ permission to adopt e-invoicing.

November 2021: Coalition new leaders confirm electronic invoice reporting system as soon as possible to fight VAT fraud; backing for EU definitive VAT system; import VAT reforms

The new German government coalition of the SPD, Free Democratic Party (FDP) and Green Party have now confirmed on 24 November 2021 plans to implement a country-wide live e-invoicing regime. It is envisaged that this will validate in real-time the creation of sales invoices by taxpayers, and then act as the forwarding channel for invoices to customers. This follows the Italian SdI model, with Continuous Transaction Controls (CTC), which in turn follows similar models adopted across South America and Asia Pacific.

If you want live updates on these changes, sign-up for our free regular global VAT/GST newsletter.

The new government has also restated its support for the proposed EU definitive VAT system, which aim to shift the EU VAT regime to a destination principle. Check VAT Calc’s global live VAT invoice transaction and e-invoice reporting tracker to see where else real-time submissions of invoices is being implemented. Our VAT Calculator can produce accurate invoice calculations and reporting globally.

The coalition has also committed to reform the import VAT rules to provide similar reverse charge relief as is common across the rest of the European Union.

Read more about German VAT in our national guide.

Germany B2G e-invoices

As per the requirements of the EU VAT Directive on e-invoicing, in April 2020, Germany mandated the acceptance of electronic invoices for Federal governmental transactions with the commercial sector, B2G.The format varies by state (Bundesland) as they adopt the legislation in their local laws. The states have the option of their own format (which should be PEPPOL compliant) or the recommended by Core Invoice User Specification (CIUS).