NAV confirms eVAT (eÁFA) pre-filled VAT returns live

Builds on RTIP real-time invoicing; initially voluntary pre-completed VAT returns and tax-code mapping service

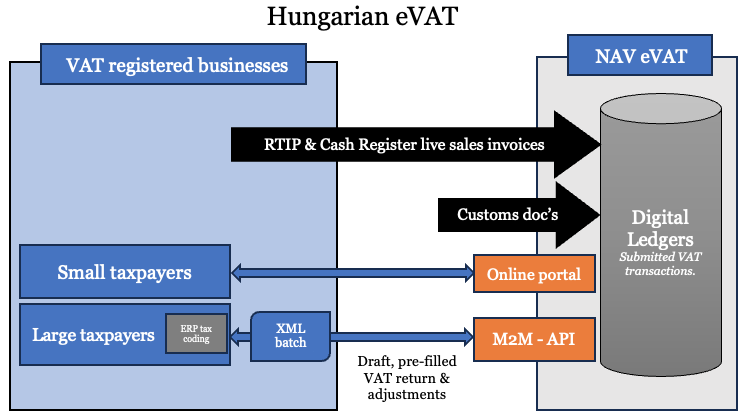

Hungary’s National Tax and Customs Administration (‘NAV’) confirmed on 1 January 2024 its new platform, eVAT, to enable taxpayers to freely access pre-filled VAT returns. The first returns may approved and submitted from February (monthly) or April (quarterly). Taxpayers may already review and interrogate data on the portal which has been gathered from: Hungarian live invoice reporting RTIP, fiscal cash registers and customs documentation. From 1 February, all functions will be available, such as changing the tax code, closing the period, preparing a draft return, pre-auditing and submitting the return.

eVAT goes beyond the OECD SAF-T model adopted in several European countries for the standardised exchange of data between the tax authorities and taxpayers. Similar to digital ledger regimes in South America and Greece’s myDATA regime, it means NAV already has a live, complete record of taxpayers’ VAT transactions. It will initially be a VAT transaction-only schema; but long term will be extended to other declaration types.

NAV also offers taxpayers a set of analytics tool to review and interrogate their VAT data set to help identify trends or errors for further investigation. Long term, as NAV can cross-check taxpayers’ transactions in eVAT, this will be particularly beneficial for taxpayers to understand misreporting of their transactions elsewhere in the supply chain.

In addition to resident Hungarian businesses, eVAT will be open to non-resident businesses with a foreign Hungarian VAT number, providing taxable supplies in Hungary.

Building on success of RTIP live invoice reporting

eVAT is based on the transactional data which taxpayers have been required to submit in real-time on the RTIP regime since July 2018. The requires near live submissions of B2B and B2C sales invoices. It also incorporates data from Hungary’s live cash-register reporting regime.

eVAT will replace the monthly obligation for a Control Statement, ‘M-forms’. This lists all domestic transactions for goods and services for VAT deductions.

NAV is proposing two routes to utilise eVAT, addressing the separate needs and preferences of small and large taxpayers. In both cases, aside from summary-level pre-filled VAT returns, taxpayers will be able to dynamically drill down into transactions to examine and issues. The current manual ÁNYK return filing option will remain in place, too.

1. Small taxpayers – free online access

Taxpayers, or their advisors, will be able to login to a online portal to access their VAT transactional data. From there, they can run basic analytics, supplement any missing transactional information, including adding new invoice transactions, in their NAV ledgers and make amendments where appropriate. They are then able to review and approve a draft VAT return.

2. Large taxpayers – M2M tax code-based assistance

Whilst pre-filled VAT returns present a free and convenient route for small taxpayers, most medium and enterprise taxpayers have more complex business models such as intra-group trading and international transactions. But dealing with these transactions on a frontend can be cumbersome and counter-productive.

To help them, NAV has developed a unique standard tax code map. Large enterprises can map their own ledgers / tax codes to this, can opt to submit full XML transaction details via a newly created API. This will be known as ‘Machine-to-Machine’ or ‘M2M’.

Once received, there is a basic data validation of two types:

- File structure and format

- Cross-checking data with other sources and analytics.

Transactions are stored in a data pool, similar to digital ledgers along with collected RTIR, cash register and customs information. After this acceptance procedure the user can move to the preparation of a draft VAT return.

In addition to then being able to access more accurate returns, this process will also automate reconciliations with NAV’s RTIP records. This will enable both sides to readily identify discrepancies, and resolve them, rather than trigger disruptive and costly audit investigations.

Since the data is being exchanged via API, this will open for the first time the opportunity for large taxpayers to interrogate NAV’s transaction records on their activities, and facilitate more readily any differences to be investigated.

Free data analytics tools

To help taxpayers fully understand and cross-check their VAT return data set, NAV is offering a suite of analytical tools.

The online portal will offer plenty pre-defined views for aggregated and itemized browsing (drill-down, slicing-dicing). This covers all three data sources that constitute a VAT declaration: invoices, cash receipts and customs declarations) These views can also be customized and saved as a personal template to use for future work. The UI also includes summary views and a pre-defined VAT analytics view to look at the flagged numbers before making a declaration submission.

The M2M API will both aggregated and itemized query operations for the clients, so they can build any analytics they want from the provided data. This can be done with tools such as PowerBI.

If a taxpayer has completed their data submission, per the analytic tools reporting, NAV is not likely to request further tax information from the tax payer in the case of an audit.

Read more in our Hungary VAT country guide.

Many thanks to Csaba Kocsis, from i-Cell Mobilsoft, in compiling this blog.