Evaluation of electronic invoicing implementations with recommendations for global tax administrations; harmonisation not possible

The Organisation for Economic Cooperation and Development has issued an initial findings report “Tax Administration 3.0 and Electronic Invoicing’ on electronic invoicing for tax authorities looking to introduce the VAT/GST control reform, or looking to update their existing e-invoicing regime.

Check our global e-invoicing tracker for country-by-country analysis.

The OECD report is based on the responses by 71 tax authorities to a survey analysing different existing solutions of e-invoicing and real-time transmission of invoice transaction data. This includes detailed case studies for Chile DTE, Hungary RTIR, Italy SdI Finland, Canada and Spain SII which have a range of post-audit and pre-clearance Continuous Transaction Controls (CTC) regimes.

Get our free VAT newsletter for international VAT updates.

Half of tax authorities operate transaction reporting

The OECD found a range of transaction reporting regimes in 46% of the 71 authorities that replied:

- VAT Listings is the obligation imposed on taxpayers to submit VAT transactional data according to a national format.

- SAF-T reporting is a specific form of DRRs based on the OECD’s standard.

- Real-time reporting is the obligation on taxpayers to transmit transactional data shortly after issuance of the invoice. The data required can be extracted from the invoice, but the invoice itself does not need be transmitted to the tax authority.

- e-invoicing is a compliance system requiring taxpayers to issue a structured e-invoice for VAT purposes. ‘Structured’ means that the e-invoice must conform to a machine-readable standard, so that it can be automatically processed. The e-invoice as a whole, or a set of data therefrom, must then be transmitted to the tax authority, prior to its issuance, as it takes place, or shortly thereafter.

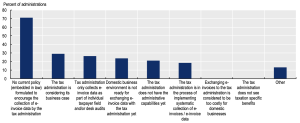

The reasons for not imposing transaction reporting varied:

Opportunity for harmonisation gone

Whilst the OECD did look at the opportunities for harmonisation of interoperability of systems between jurisdictions to help businesses comply, it quickly concluded this would not be possible. The need for local requirements and objectives meant that tax administrations have introduced many varying systems. The problem with e-invoice standards is that there are so many. Among the well-known standards are the UN/CEFACT cross-industry invoice (CII), the OASIS UBL (ISO/IEC 19845) International Standard, and the European standard on e-invoicing (EN 16931) which was developed and published by the European Committee for Standardisation (CEN).

The impacts of this uncoordinated the development of different versions of electronic invoicing holds lessons for the importance, where possible, of international collaboration on the development of systems which apply across borders to minimise the emergence of significant and persistent burdens which can impact both business and tax administrations and which can potentially become unsustainable in the light of changing business models.

E-invoice considerations; SAF-T update

The report does present a set of considerations that tax administrations may want to take into account in exploring the possible introduction or reform of electronic invoicing. For example, the role of digital signatures to secure the authenticity, integrity and non-repudiation of e-invoices. Also, the role of Peppol

It als provides a brief update on initial work undertaken on the latest state of play with the implementation of the OECD Standard Audit File for Tax which is being used by some administrations as part of periodic transaction reporting for VAT.

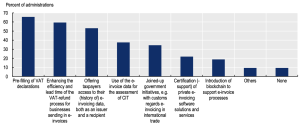

Future e-invoicing and other digital reporting initivites – pre-filled VAT returns

The OECD report also assessed the tax authorities’ plans for introducing e-invoicing and similar measures. The results showed that pre-completed VAT returns were highest on tax administrations’ minds:

EU e-invoicing plans to be revealed November 2022

EU VAT in the Digital Age reforms include a channel for harmonised Digital Reporting Requirements (DRR) and Continuous Transaction Controls (CTC)

by EU states. This grew from the 2020 EU Tax Action Plan proposals for a fairer and more efficient EU tax regime.